Last year Nathan at winnerstradingedge.com wrote a brilliant piece which you can find here talking about Why Nial Fuller’s Method Doesn’t Work (referring specifically to his risk models).

In this article, he is responding to Nial’s claim that the superior forex risk management system is to risk a fixed dollar amount per trade. It should be noted Nial’s main claims were 1) a fixed dollar amount could get you out of a DD (drawdown) faster when winning, while 2) it would take longer to get out of the same DD if you used a fixed % equity model.

Nathan decides to demonstrate in two scenarios how a fixed % equity model is actually far superior. Nathan’s data shows clearly using a fixed dollar amount actually hurts you both in DDs (drawdowns) and during winning streaks.

I completely disagree with Nial Fuller and have always endorsed a fixed % equity risk model as being far superior. I will demonstrate this later with data and several scenarios. But first, onto Nathan’s results.

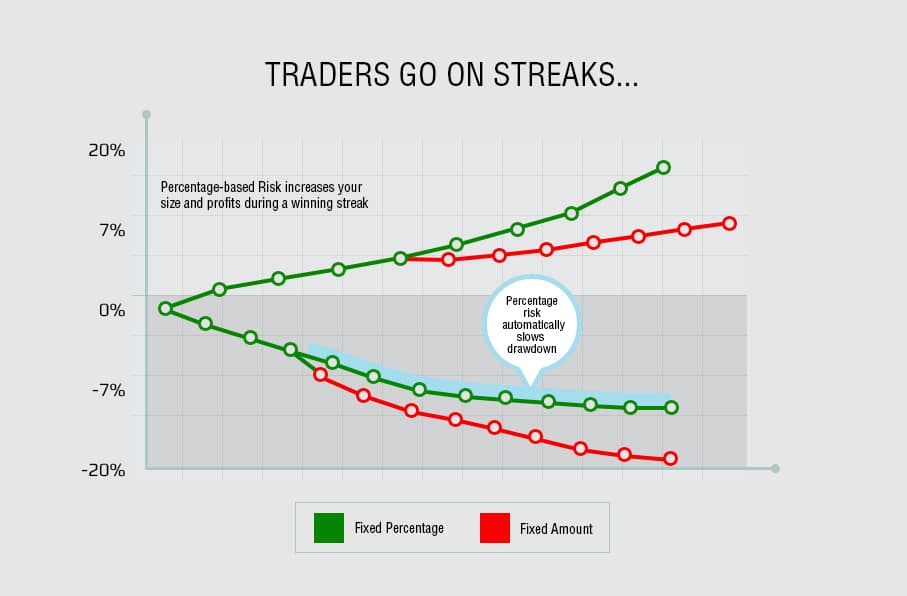

In this chart below, he shows two accounts each with the same starting balance of $10000. The two accounts were either using a 2% risk per trade method (representing the fixed % equity model) vs. the fixed dollar amount (risking $200 per trade each trade). Below is the graph showing the performance of the two models.

Nathan in his experience noticed how traders go on winning streaks. He thus tested two scenarios, whereby the traders go on either a 10 win-streak, or a 10-loss streak. The green line is our model (fixed equity % model). The red line is Nial’s model (the fixed dollar risk method).

During a winning streak, our fixed % equity model pulls away from Nial’s fixed dollar amount and continues to gain further as it goes on. This happens around trade 5 and continually separates further after each winning trade.

For the losing streak, our fixed % equity model again outperforms Nial’s, by losing less each trade, thus protecting your capital.

After Nathan published this data highlighting the differences, people on both sides disagreed. But nobody was providing any more data to back up either side. We at 2ndSkiesForex decided to run the numbers ourselves and further demonstrate how a fixed % equity model was far superior.

The first forex risk scenario we looked at was a 10 win trade recovery after the 10 loss series Nathan presented above. Here is how the data plays out below.

After 10 losses, Trader A goes on to win the next 10 using the fixed % model:

-As per the chart above, Trader A has a balance of $8171 at trade 10. This continues below-

$8334.42 at trade 11

$8501.10 at trade 12

$8671.12 at trade 13

$8844.54 at trade 14

$9021.43 at trade 15

$9201.85 at trade 16

$9385.88 at trade 17

$9573.99 at trade 18

$9765.06 at trade 19

$9960.36 at trade 20 for fixed 2% rule

After After 10 losses, Trader B goes on to win the next 10 using the fixed % model:

-As per the chart above, Trader B has a balance of $8000 at trade 10

-Since the math is easy, at trade 20 Trader B has a balance of $10000, for a whopping .4% difference.

Now in comparing the numbers as a whole over these last three scenarios, lets look at the following three facts:

1) During the first 10 win UD (updraw), you get +1.58% BETTER performance (more upside) using a fixed % model

2) During a 10 loss DD (drawdown), you get +1.71% BETTER performance (or lesser DD) using a fixed % model

3) During the next 10 win UD (updraw) you get -.4% LESSER performance (or lesser gains) using a fixed % model

So in two out of the three forex risk scenarios above, the fixed % equity model outperforms the fixed dollar amount. The total edge is +2.89% over the fixed dollar amount using the fixed % equity method.

But lets take this a few steps further and lay out the other 4 scenarios from here to see which performs better. They are;

Scenario 1 = 10 more straight wins from trade 20

Scenario 2 = 5 more straight wins from trade 20

Scenario 3 = 5 more straight losses from trade 20

Scenario 4 = 10 more straight losses from trade 20

Scenario #1: (10 more straight wins from Trade 20, or T20)

Trader A Balance = $9960.36

Trader B Balance = $10000

After 10 more trades (T21-T30), the fixed 2% model will have a balance of $12143 while the fixed dollar model will have a balance of $12,000. Summed up, the fixed % model has $143 MORE in profit, or a 1.2% GREATER gain. Hence the fixed % model wins this scenario.

Scenario #2 (5 more straight wins from trade 20)

Trader A Balance = $9960.36

Trader B Balance = $10000

After T25 (or 5 more straight wins), fixed 2% model has a balance of $10998.69 while the fixed dollar amount has a balance of $11,000, or a whopping $1.31 more, which is only a .01% gain over the fixed % model. Pretty weak difference. But a win nonetheless for the fixed dollar model.

Scenario#3: (5 more straight losses from trade 20)

Trader A Balance = $9960.36

Trader B Balance = $10000

By T25, the fixed % model has a balance of $9002.78, while the fixed dollar amount has a balance of $9000. Summed up, the fixed % model has $2.78 MORE in profit, or a .03% gain over the fixed dollar amount. A small difference, but nonetheless a win for the fixed % model.

Obviously from here the answer gets much uglier for the fixed dollar amount model as this progresses, but here are the numbers below.

Scenario #4: (10 more straight losses from trade 20)

Trader A Balance = $9960.36

Trader B Balance = $10000

By T30, the fixed % amount has a balance of $8136.84, while the fixed dollar amount has a balance of $8000. So the fixed % model has $136.84 MORE in capital, or a 1.7% gain over the fixed dollar amount.

When you tally up the 2 scenarios by Nathan, plus the 4 we just ran, the score is 5-1 with the fixed % equity model being the far superior model.

Here are the numbers and scenarios summarized below;

Scenario A (Nathan’s scenario – 10 wins from 10k) = +1.58% better performance for fixed % equity model

Scenario B (Nathan’s scenario -10 losses from 10k) = +1.71% better performance for fixed % equity model

Scenario 1 (as per my description above) = +1.2% better performance for fixed % equity model

Scenario 2 (as per my description above) = -.01% worse performance for fixed % equity model

Scenario 3 (as per my description above) = +.03% better performance for fixed % equity model

Scenario 4 (as per my description above) = +1.7% better performance for fixed % equity model

This comes out to a grand total +6.21% better performance for the fixed % equity model across 6 scenarios.

Translation

This shows a huge advantage using the fixed % equity forex risk management model which is clearly far superior to the fixed dollar amount method. This is only across 20-30 trades using any one scenario above. The more trades this gets applied to, the better the performance. Over a traders lifetime of 500, 1000, or 5000+ trades, this edge becomes exponentially superior.

Keep in mind, you cannot do any risk of ruin calculations using a fixed dollar amount, however you can using our % equity model. Anyone using Nial’s fixed dollar model is simply throwing money away over time.

This should end the debate between which forex risk management system is the better model. Clearly the fixed % equity forex risk management model wins by a Mortal Kombat Fatality.

I would like to state I am welcome to see evidence to the contrary if/when it is presented, as I am totally open to seeing it.

Make sure to share this “how much to risk per trade” article as it discusses a critical topic for your trading. But more importantly – leave a comment whether you agree or disagree, and why.

This is not always true. In the case you have a large win followed by a loss, followed by a large win, followed by a loss etc…. In this scenario fixed $ outperformed massively. Your above article is true but only for the limited examples above of long streaks of gains or losses.

Hello Stuart,

This situation is so vaguely described, there is no way to demonstrate your statement being correct or incorrect.

So unless you have a mathematical model to demonstrate this, what you are saying is really just thin air.

FYI – nobody has a trading model or history like the one you describe above. Why? Because wins and losses are randomly distributed – they’ll never come out in a long series the way you described them. Traders will go on streaks of wins and losses, and have mixes of them in various combinations in between.

So in essence – what you are describing above cannot be true.

But…if you really believe the fixed % model does not outperform the fixed $ model – take the pepsi challenge – walk into 50 hedge funds, prop firms and bank desks. Then ask them what the majority of them are using for their risk models.

I’m quite confident the fixed % model will overwhelmingly win that one.

But thanks for sharing.

Kind Regards,

Chris Capre

Brilliant Chris! Absolutely brilliant!

I have read almost all of your articles and seen almost all of your videos. Your trading course is such a masterpiece! My most well invested money ever!

I am a beginner in FX and I am very glad I found your course. Learn the skill properly and early will save me both time and money. A golfer who learns to swing incorrect from the beginning will have major problems to fix it later. A bad behavior is hard to change. I believe it’s the same for traders.

Articlewise, I certainly agree with you and Natan. Just do the math! A fixed % equity will follow your learning curve. It’s working parallell with your results. If you perform well you increase your money you risk and vice versa, which I think you are deserved to do. If perform bad you decrease it, just by the ”Chris” book. Why should you lower your percentage risk if you are increasing your skill, knowledge and experience? It just doesn’t make sense?

An alternative for the safe minded trader could be to go fixed % if your are on the negative side of 10 000 $ and fixed amount if above. You will then risk the least amount of all alternatives.

Once again thank you for all your work!

/Alexander

Great article Chris! This should put an end to the discussion once and for all. Of course it’s up to everyone what they want to use.

To completely wipe out an account of 5000$ when trading with a fixed risk of 100$ on each trade would need 50 losing trades in a row.

Using 2% risk instead would still leave you with 499$ in your account after 114 losing trades in a row.

Using only 1% risk would leave you with 495$ in your account after a massive 230 trades loosing streak.

Should be pretty much impossible to pull that off. 🙂

I am not sure why this was even argued or in doubt. Exponential growth using a fixed % will always be higher than linear. I would love to grow my account at 1% a day rather than $100/day

Tis a good question Chubbly. If someone fails to do the math, then its easy to be misled by those not doing the numbers properly. Hopefully this highlights the difference as to which model keeps money in your pocket, and which throws it away.

Kind Regards,

Chris Capre

numbers never lie. This is very important- I am glad you pointed this out so traders can get educated about this subject and possibly this can build and keep them in the “game”.

Hello Sam,

Indeed, the numbers do not lie and this is critical. Hopefully traders won’t be misled by poor models that actually give money away.

Kind Regards,

Chris Capre

“a +6.21% better performance for the fixed % equity model across 6 scenarios.” The numbers clearly spell it out.

Agreed and appreciated

Hello Sean,

Yes, a +6.21% difference using our model, and that is only across 20-30 trades. Imagine that difference over 500 trades after a few years? Quite a difference.

Kind Regards,

Chris Capre

Risking dollar per trade also seems to effect equity threshhold in a negative way.. it seems % is far superior in a way its just 2% or 5% risk On a trade no matter the equity but when risked something like 1k or 2k which is equivalent to 2 or 5% seems to effect emotions and bring up ideas like I can pay my rent with 1k I can buy this I can buy that etc etc.

Hello Saif,

Yes, using the dollar per trade model will effect your equity threshold in a negative way. And yes, the % model is a far superior way to manage your risk.

Kind Regards,

Chris Capre

Superb Article !!!!! Finally I can realise how significant the difference is, thank you Chris for this eye-opening article !!! It really can show the difference between a successful trader and a losing ones xD

HQ.

Hello HQ,

Yes, the math is quite clear when you start to tease out the data – it shows how huge a difference this can be over time and a lot of trades.

But glad you found this an eye opening article and how one model shows the difference between a winning trader and a losing one.

Kind Regards,

Chris Capre

Thanks for crunching the numbers for us Chris.

I tried using the fixed dollar amount as well as the fixed % amount so I already know from experience that fixed % is far superior.

This article really puts things into perspective.

Hello Paul,

Yes, this is what a ton of students and traders are telling me – that they tried it (fell for it) and realized the fixed % amount was making more money while protecting more capital.

So am glad you recognized this as well.

Kind Regards,

Chris Capre

Hi Chris,

Forex smart tools will also do the same simulation and 9 out of 10 times fixed percentage wins. It’s also a handy tool for calculatin percentage risked.

Hello Justin,

Thanks for sharing this as I like their products. Indeed – in a huge majority of simulations, fixed % wins.

Kind Regards,

Chris Capre